Making Your Retirement Savings Last: Calculating Income and Spending with Confidence

Your retirement funds can sustain you for life when you know how to generate reliable income from your savings, prepare for various financial scenarios and longevity outcomes, and develop the assurance to shift from accumulation to distribution mode.

Although retirement is something most people eagerly anticipate, fewer than half of Americans approaching retirement have actually determined how much they’ll need to save. Yet there’s an even more intriguing paradox: numerous individuals who’ve been disciplined savers find themselves facing a completely unexpected obstacle—they can’t bring themselves to actually use their money.

Whether you envision exploring far-off places, creating memories with grandkids, pursuing hobbies, or supporting causes close to your heart, making your nest egg stretch across your entire retirement requires careful strategic thinking.

It also demands something less tangible: the self-assurance to move from decades of accumulating wealth to actually living off what you’ve created.

The Toughest Challenge in Retirement? Shifting to Spending Mode

Following three or four decades of being praised for putting money away, you’re suddenly expected to reverse course. This pivot creates what behavioral finance experts describe as “spending anxiety”—the worry that each withdrawal could be the beginning of depleting your resources entirely.

This fear has legitimate roots. Unlike your employment years with their predictable paychecks, retirement income sources can feel more uncertain, prompting some people to be excessively conservative with withdrawals.

Here’s the paradox: being overly cautious often results in retirees spending far less than they could, forfeiting experiences and pleasures they’ve worked toward (and budgeted for).

Achieving a successful retirement transition goes beyond simply knowing your account balances—it means understanding exactly how much steady income your accumulated savings can generate. This understanding converts worry into confidence, empowering you to genuinely enjoy retirement instead of simply sitting on funds you’re hesitant to access.

Determining Your Retirement Income Requirements

Begin with your lifestyle blueprint

Before getting into retirement calculators and safe withdrawal percentages, start by clarifying what you actually envision for your retirement years. Reflect on questions like:

- Will extensive travel fill your early retirement, or do you prefer remaining close to home?

- Are you planning to downsize, or stay in your current residence with possible modifications as you age?

- Will you move closer to family members or to a region with lower living costs?

- What interests or pastimes do you want to explore that might require financial investment?

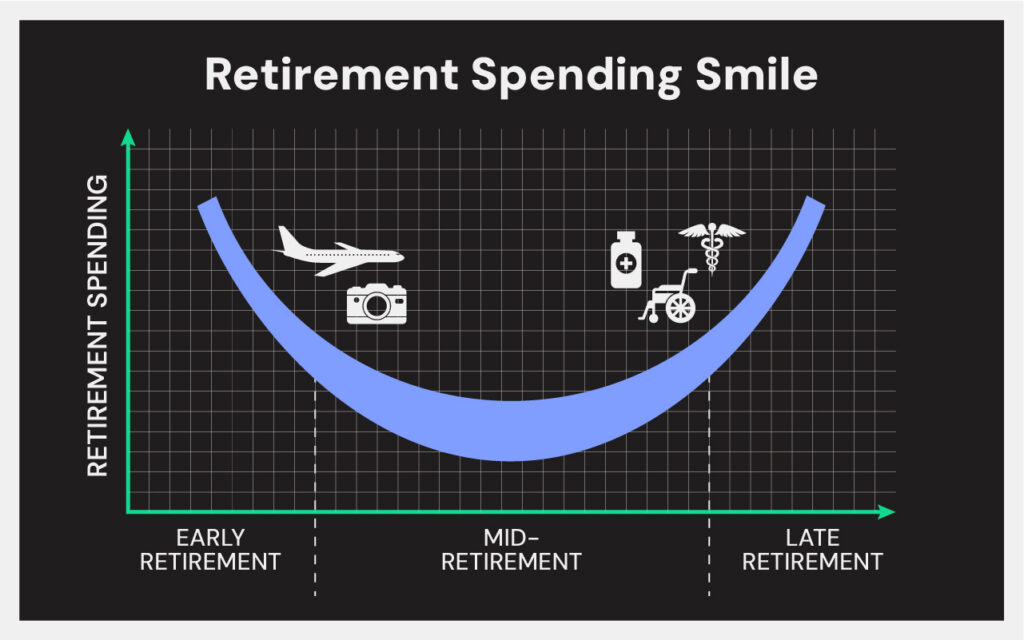

Your vision matters significantly because retirement spending typically follows what researchers describe as the “retirement spending smile.”

Deploy retirement calculators wisely

Retirement calculators offer valuable insights into both your potential savings targets and how long those savings might sustain you.

Check out the calculators on this page to compare tax-deferred to taxable accounts, discover annuity tax advantages, and estimate how long your money will last in retirement.

That said, avoid depending on just one projection. Model various possibilities:

- Optimistic scenario: Strong market returns, living to typical life expectancy

- Conservative scenario: Early retirement market decline, longevity to 95 or beyond

- Realistic scenario: Moderate returns and lifespan falling somewhere between

The 4% Rule: Understanding Its Purpose and Constraints

A widely recognized straightforward method for sustainable retirement withdrawals involves the 4% Rule, which recommends taking out 4% of your starting retirement balance annually, with increases to match inflation.

Here’s a practical example: Beginning retirement with $1 million, you’d take $40,000 the first year. Year two, you’d inflation-adjust that $40,000—with 3% inflation, that becomes $41,200. Each subsequent year adjusts the previous amount for current inflation rates.

This guideline seeks to establish sustainable income while maintaining principal, drawing from historical market data across 30-year timeframes.

Yet the 4% Rule comes with critical caveats:

- It assumes a 30-year retirement period (yours might need to last longer, particularly with early retirement)

- It overlooks spending fluctuations and tax implications

- Retiring during market downturns creates “sequence of returns risk”—significant early portfolio losses combined with ongoing withdrawals can drain savings much faster than historical patterns suggest

- It doesn’t incorporate pension payments, Social Security, annuities, or other guaranteed income you might receive

Advanced strategies employ dynamic withdrawal approaches that respond to portfolio performance and spending needs. You might take 5% during robust market years and 3% during downturns, or increase spending early in healthy retirement years while reducing it later. These adaptive methods can extend portfolio longevity while maximizing enjoyment during your most active years.

Creating a Multi-Layered Income Approach for Lasting Retirement Funds

When considering whether your money will last, the answer hinges not only on accumulated savings but on how strategically you convert those savings into reliable income.

Effective retirement transitions involve establishing diverse income sources that function cohesively, minimizing dependence on any single source while extending portfolio sustainability.

Picture it as constructing a financial base supported by multiple columns. When one source underperforms or encounters difficulties, others maintain your overall stability.

Recognizing Your Available Income Sources

Social Security Benefits

Create the cornerstone for most American retirees, delivering guaranteed, inflation-protected income throughout life. When you begin claiming—anytime from 62 to 70—permanently determines your monthly amount. For couples, strategically timing each spouse's claim can dramatically influence both present household income and future survivor benefits.

Pension Income

For those who have it, this adds another guaranteed income layer. Pension holders must decide between lump-sum distributions versus monthly payments, plus whether to include survivor benefits for spouses.

Retirement Accounts

Accounts such as 401(k)s, IRAs, and 403(b)s hold the wealth you've built throughout your career. Since many use pre-tax contributions, retirement withdrawals generally count as taxable income. These accounts allow flexibility in withdrawal amounts and timing, but demand careful oversight to ensure longevity, especially given their exposure to market fluctuations.

Personal Savings and Investments

Savings and investments in taxable accounts add extra flexibility. These resources typically come without withdrawal penalties or limitations, making them valuable for covering unexpected costs or seizing opportunities.

Annuities with Lifetime Income Riders

These can bridge the shortfall between guaranteed income from Social Security or pensions and actual living costs. Similar to many retirement accounts, annuities accumulate value tax-deferred, with income taxes generally applied to earnings upon withdrawal. Converting part of your savings into guaranteed* income streams delivers consistent payments on a predictable schedule to help manage expenses, regardless of lifespan or market conditions.

Planning for Healthcare Expenses in Retirement

Healthcare costs represent one of retirement’s biggest uncertainties. A healthy 65-year-old couple retiring in 2025 might spend approximately $588,000 on healthcare throughout retirement—$275,000 for men (projecting an 88-year lifespan) and $313,000 for women (projecting a 90-year lifespan).¹

Medicare addresses many primary needs, yet premiums, deductibles, and services not covered mean retirees must carefully account for health expenses when developing sustainable income plans.

Long-term care presents a distinct challenge. Medicare doesn’t cover the majority of long-term care expenses.

Whether you choose to self-fund, buy long-term care insurance, or utilize an optional rider on an annuity or life insurance policy to help address these costs, incorporating these potential needs into your income strategy is crucial.

Strategic Tax-Efficient Withdrawal Sequencing

The accounts you draw from—and the order you tap them—can significantly extend your savings’ lifespan, determining whether you feel concerned or confident.

Financial planners often recommend this withdrawal sequence2:

- Taxable accounts (brokerage accounts, savings)

- Tax-deferred accounts (traditional IRAs, 401(k)s)

- Roth accounts last (Roth IRAs, Roth 401(k)s)

Collaborating with your financial professional to evaluate various withdrawal sequences could potentially preserve tens of thousands in taxes across a 30-year retirement.

Steering Clear of Common Retirement Income Pitfalls

Several typical mistakes can derail your transition from building savings to drawing retirement income.

Underestimating longevity: Retiring at 65 means there’s a strong probability that at least one spouse in a married couple will survive into their 90s. Planning only to 85 could leave you financially short by ten years or more.

Ignoring inflation: Even moderate 2-3% yearly inflation accumulates substantially over time. What requires $50,000 today will need roughly $90,000 in two decades at 3% inflation. Your income approach must maintain purchasing power.

Taking excessive risk—or insufficient risk: An overly cautious portfolio might not produce adequate growth to support withdrawals spanning 30+ years. Conversely, excessive risk-taking, particularly early in retirement, exposes you to sequence-of-returns danger.

Overlooking taxes: Many retirees are caught off-guard by how much retirement income faces taxation. Social Security income may be taxed, traditional IRA distributions are completely taxable, and investment income increases your tax burden. Consider your net, after-tax income during planning.

Transforming Calculations into Retirement Assurance

Understanding the numbers matters. But genuine retirement confidence emerges from converting those calculations into a dynamic income plan addressing both practical requirements and emotional well-being.

Grant yourself permission to spend

Your retirement savings weren’t meant to be preserved indefinitely—they’re designed to fund the retirement you’ve envisioned.

A straightforward approach to feeling more comfortable with withdrawals is organizing your money into three categories:

- Income now (next 1-5 years)

- Income soon (years 5-15)

- Income later and legacy (15+ years and beyond)

Viewing your savings this way makes withdrawals less intimidating. You’re drawing from the “now” category, while the others continue growing in the background to support future years.

Establishing Retirement Confidence Through Guaranteed Income*

One highly effective method for easing the saving-to-spending transition involves establishing a guaranteed* income foundation covering your essential expenses. Knowing your basic needs are met regardless of market performance grants you flexibility with remaining assets.

A guaranteed income foundation typically includes:

- Social Security benefits (optimized for maximum benefits)

- Pension payments (when available)

- Annuities with lifetime income riders

Once essentials are covered by guaranteed sources, market volatility anxiety diminishes considerably. You’re not monitoring your portfolio balance daily, questioning whether you can still afford necessities or healthcare. Instead, you’re making deliberate decisions about discretionary spending—travel, gifts, hobbies—with the knowledge that your foundation remains secure.

Move Forward

Whether you’re just starting to build your nest egg or you’ve already made significant progress toward funding your golden years, now is the time to consult with your financial professional to assess how long your retirement savings will last—and to develop the confidence to truly enjoy it.

Key Takeaways – Look to your financial professional to help:

- Calculate realistic income needs aligned with your specific retirement vision and spending patterns

- Identify gaps between guaranteed income sources and lifestyle expenses

- Model different scenarios including market downturns and longevity beyond expectations

- Explore income diversification strategies including annuity options with lifetime income guarantees*

- Develop a tax-efficient withdrawal strategy that maximizes your after-tax income

- Create an annual review process to adjust your plan as circumstances change

The objective isn’t merely making your money last—it’s ensuring your retirement fulfills everything you’ve worked toward, free from constant worry about whether you can afford to actually live it.

A successful retirement transition occurs when calculation meets confidence, when your spreadsheet transforms into sustainable paychecks, and when you grant yourself permission to be the beneficiary of your own lifelong discipline and hard work.

1 2025 Milliman Retiree Health Cost Index

* Annuity guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

ULPUB-007 02-26

Related Posts

AI vs. Financial Professional: Who Should You Trust With Your Financial Plan

AI vs financial professional: Which should you trust with your financial plan? Understand what AI does well, where it falls short, and why pairing it with a financial professional leads to stronger outcomes.

Steps to Retirement: First Things to Consider When Planning

Learn the first steps to retirement planning, including understanding expenses, reviewing income sources, spotting gaps, and exploring ways to help savings last.

Why Fixed Indexed Annuities Still Stand Out in a Low-Interest Rate Environment

Interest rates dropping? See why Fixed Indexed Annuities still shine with principal protection, tax-deferred growth, and lifetime income options.